COVID-19 impacts on hostel performance: April update

Keep up-to-date with WYSE webinars >

By Kelsey Fenerty, STR

April marked the first full month of COVID-19-related lockdowns, and hostel and hotel data declined accordingly. Many properties temporarily closed, either by their own initiative or by government mandate, while others remained open to house stranded travellers, key workers and any other sources of remaining demand. The UK’s particularly stringent lockdown rules closed virtually all hostels in Edinburgh and London, leading to a temporary halt to hostel reporting in those markets.

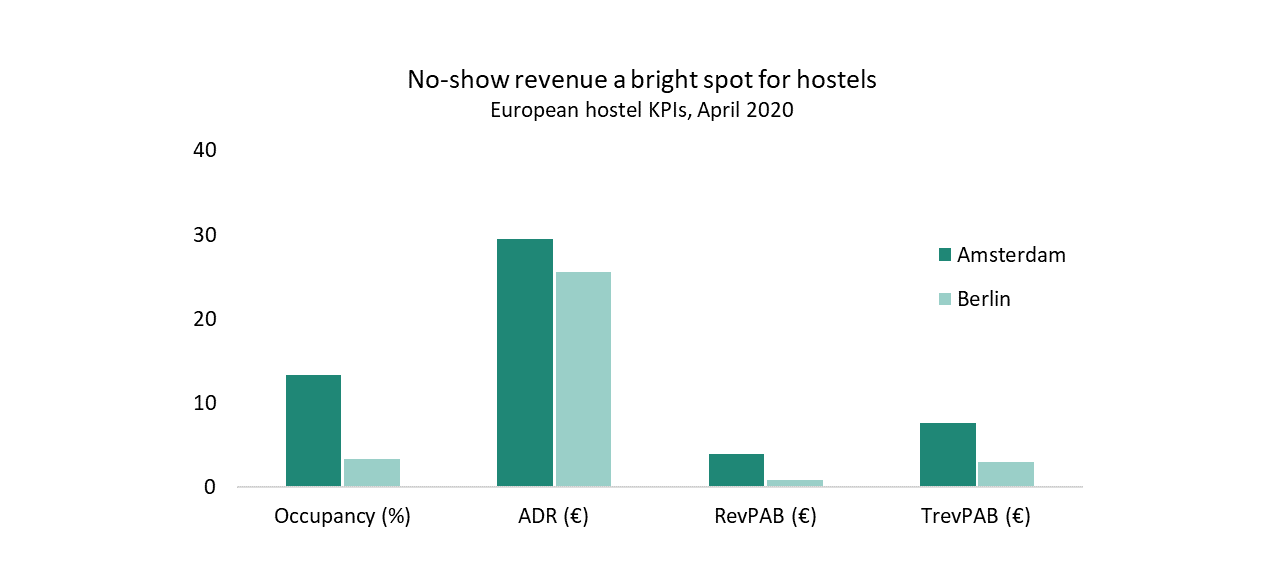

No-show revenue and cancellation fees buoy hostel performance

In STR’s remaining two hostel markets, Amsterdam and Berlin, the situation remained grim. While March occupancy fell approximately 66% in both markets, April occupancy declined 85% in the Netherlands’ capital city and 96% in Berlin.

A small relief for hostels came in the form of no-show revenue. Berlin hostel Average Daily Rate (ADR) rose 11% in March and April despite sizeable declines in occupancy. Amsterdam hostel rate declined 28% in April, but the loss could partially be attributed to refunds of cancellation fees accrued in March, when ADR increased 33%. On balance, Amsterdam ADR fell by €11 in April but maintained the highest ADR among STR’s hostel markets.

Hostels and hotels struggle equally

By the end of March, border closures, social distancing requirements and stay-at-home orders had effectively ended normal travel. Much of the remaining demand – Amsterdam hostels and hotels sold a combined 78,990 room nights and Berlin accommodations sold 131,577 room nights in April 2020 – came from stranded travellers, key workers and locals self-isolating, moving or otherwise in need of temporary accommodation.

As a result, demand fell more than 89% across all accommodation types. Midscale and Economy hotel rooms, which remained affordable but without the social distancing concerns associated with hostels, fared (relatively) well—not just in Amsterdam and Berlin but across all of Europe.

Don’t expect much from May

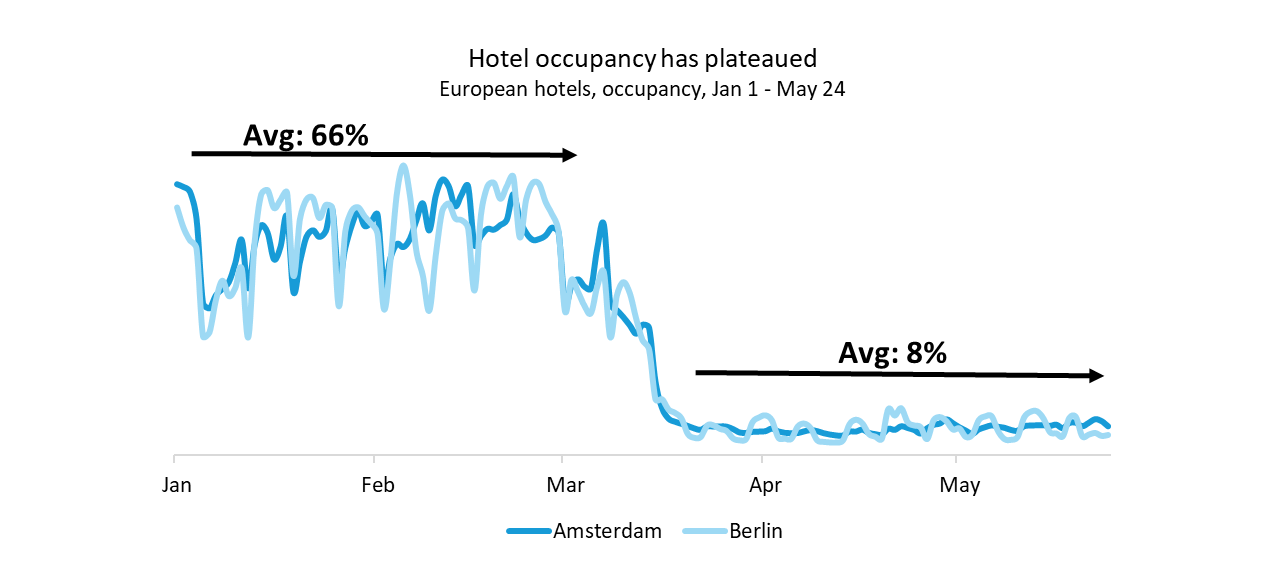

Looking at daily hotel data through May 24, 2020, allows insight into what hostels can expect when May monthly data is released in a few weeks.

First, don’t expect much to change between April and May performance. In Amsterdam and Berlin (and the rest of Europe), hotel occupancy remained low at less than 10% for all of April and most of May.

Second, this sustained level of occupancy suggests this is the worst things will (or can?) get, and future changes to occupancy should trend slightly positively.

Finally, these low occupancies coincide with lockdowns. As lockdowns start to lift at the end of May and into June, it is reasonable to expect demand to resume, albeit very slowly.

Conclusion

Much like the pandemic itself, hostel and hotel performance in April was unprecedented, and recovery likely will stretch through 2022. Leisure travel, and especially domestic leisure travel, will be first to resume; attracting that segment will be key to an early recovery.

With their affordability, authenticity, and adaptability, hostels are well-positioned to find those travellers.

Interested in More?

STR has created a dedicated page for all hotel performance analysis around COVID-19.

For more information regarding the hostel industry, please contact Patrick Mayock at pmayock@str.com.

About STR

STR provides premium data benchmarking, analytics and marketplace insights for global hospitality sectors. Founded in 1985, STR maintains a presence in 15 countries with a corporate North American headquarters in Hendersonville, Tennessee, and an international headquarters in London, England. STR was acquired in October 2019 by CoStar Group, Inc. (NASDAQ: CSGP), the leading provider of commercial real estate information, analytics and online marketplaces. For more information, please visit str.com and costargroup.com.

Join WYSE Travel Confederation

If you’d like to join WYSE Travel Confederation and benefit from new connections, free access to industry research, informative webinar sessions, discounts on industry events and brand exposure within the youth and student travel industry, click below to view our membership options and find out more.