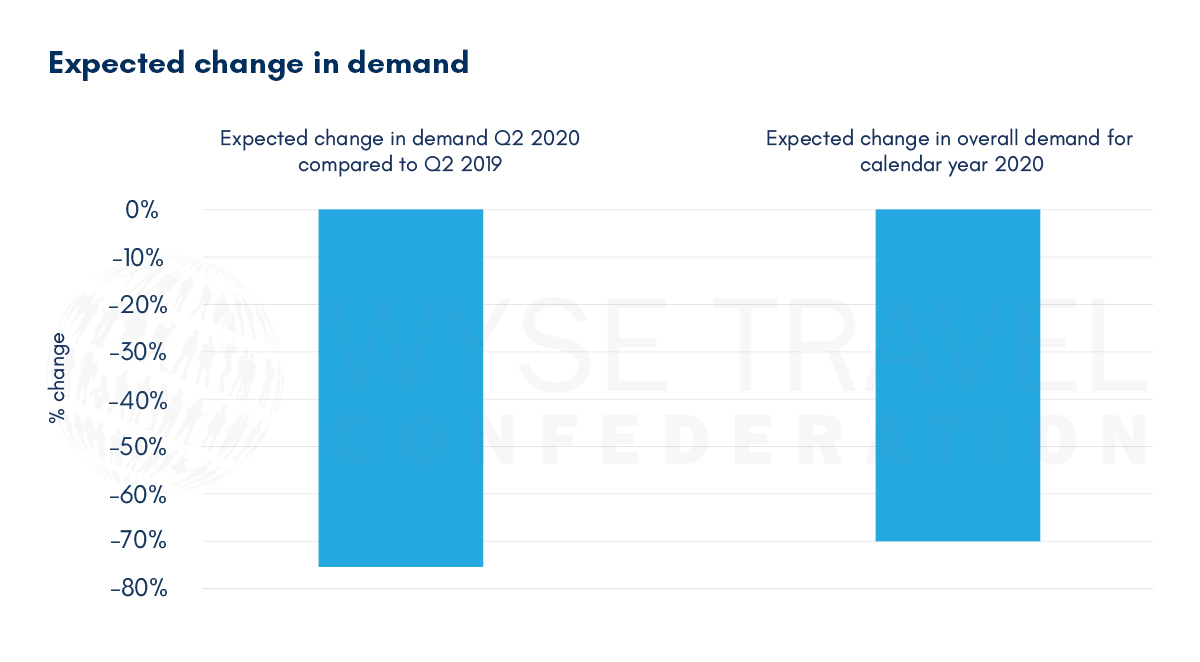

The business outlook of travel and tourism companies continues to worsen, according to findings of WYSE Travel Confederation’s third COVID-19 Travel Business Impact Survey.[1] For the second quarter of this year, the average expected change in demand relative to the same period last year is -76%. For 2020 as a whole, respondents expect to see, on an average, a 70% decrease in demand. In this May edition of this survey series we take a look at the actions that respondents would like to see governments taking to address the crisis, including the provision of financial assistance, investment in public health and establishing global standards.

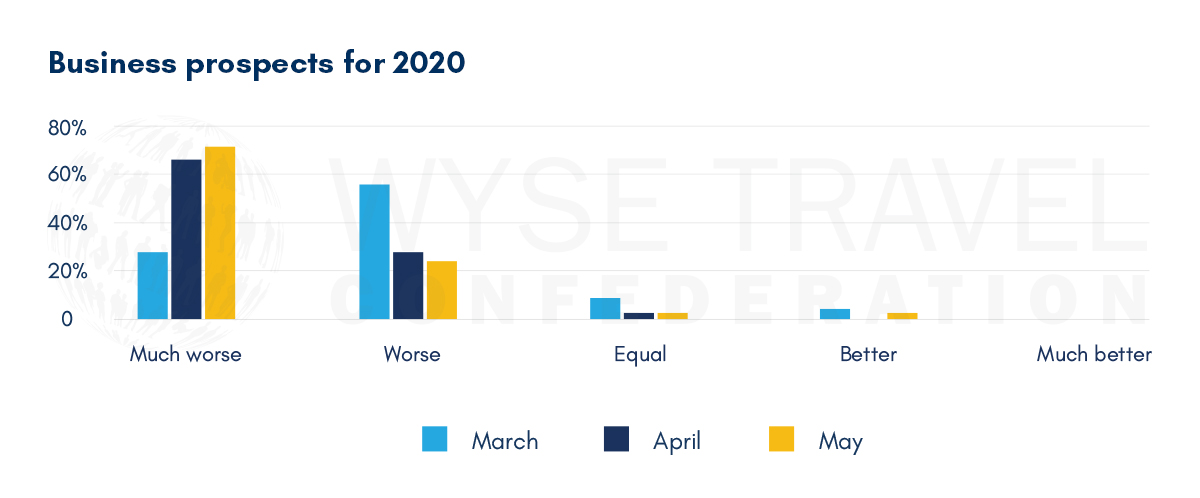

Business prospects for 2020

Business prospects for 2020 continue to worsen. The proportion of respondents expecting things to get much worse as a result of COVID-19 has gone from 28% in March to 72% in May. Hardly any respondents in May expected business prospects for 2020 to get better or even to remain the same.

Demand

With travel restrictions in place across the globe, it is not surprising that demand continues to fall. The average expected change in demand for Q2 2020 relative to Q2 2019 was -76%. For 2020 as a whole, respondents expect to see an average 70% decrease in demand for their primary product/line of business.

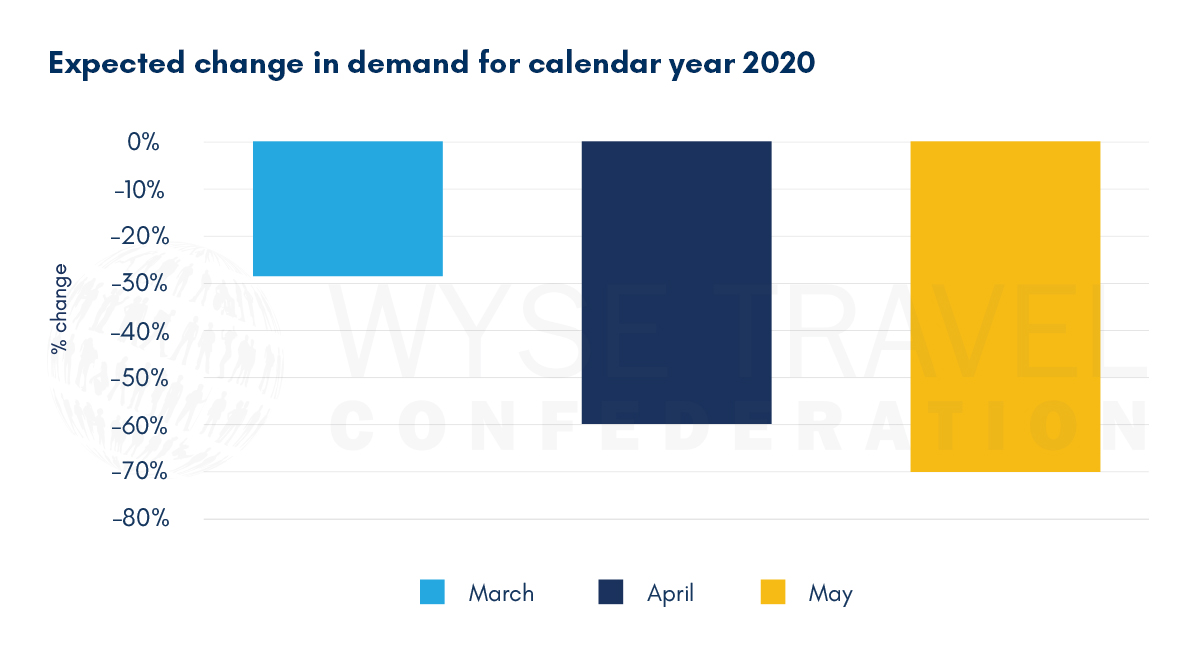

Between March and April 2020 there was a sharp fall in expected demand for the calendar year, from just under -30% in March to –60% in April. In May, results indicate a stabilisation in expectations, although continue to reflect a severe reduction in demand.

Different areas of youth and student travel show some variation in expectations for both Q2 2020 and the whole of 2020. The least pessimistic are technology providers. Gap year companies have been least affected compared to others but are expecting a sharper decline over the rest of 2020. The most severely affected businesses in youth and student travel in Q2 are transportation, insurance and accommodation providers.

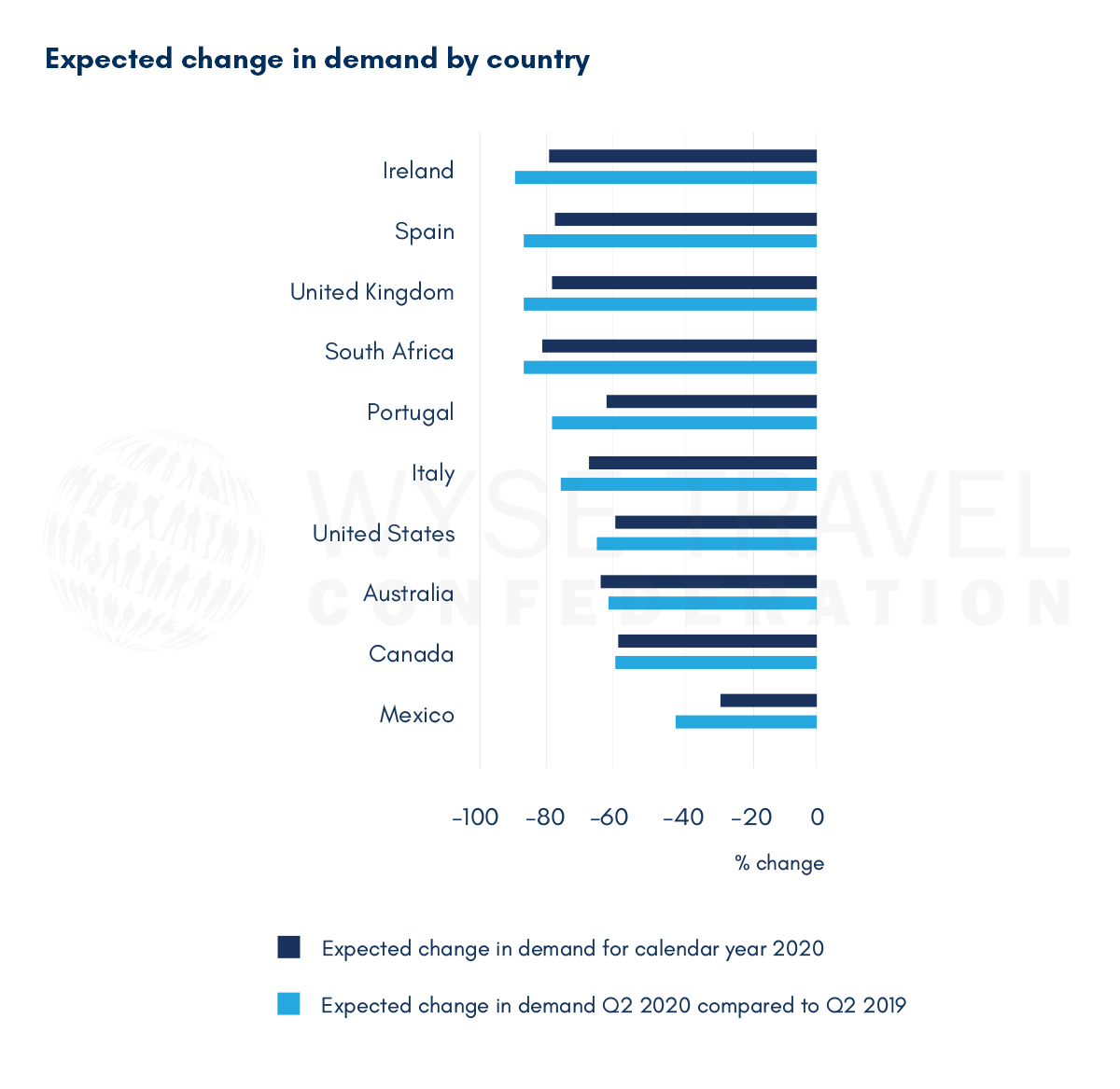

At country level there are some differences in demand. Respondents based in Ireland have been hardest hit in Q2, followed by Spain and the UK. Italy, the first European country to be severely hit by the virus, is expecting slightly stronger demand in Q2 this year than other European countries. Portugal, which has so far done a good job of containing COVID-19 deaths, is the most optimistic European country in terms of anticipated business prospects for 2020. North American countries and Australia are expecting slightly better results for both Q2 and the whole of 2020 than their European counterparts.

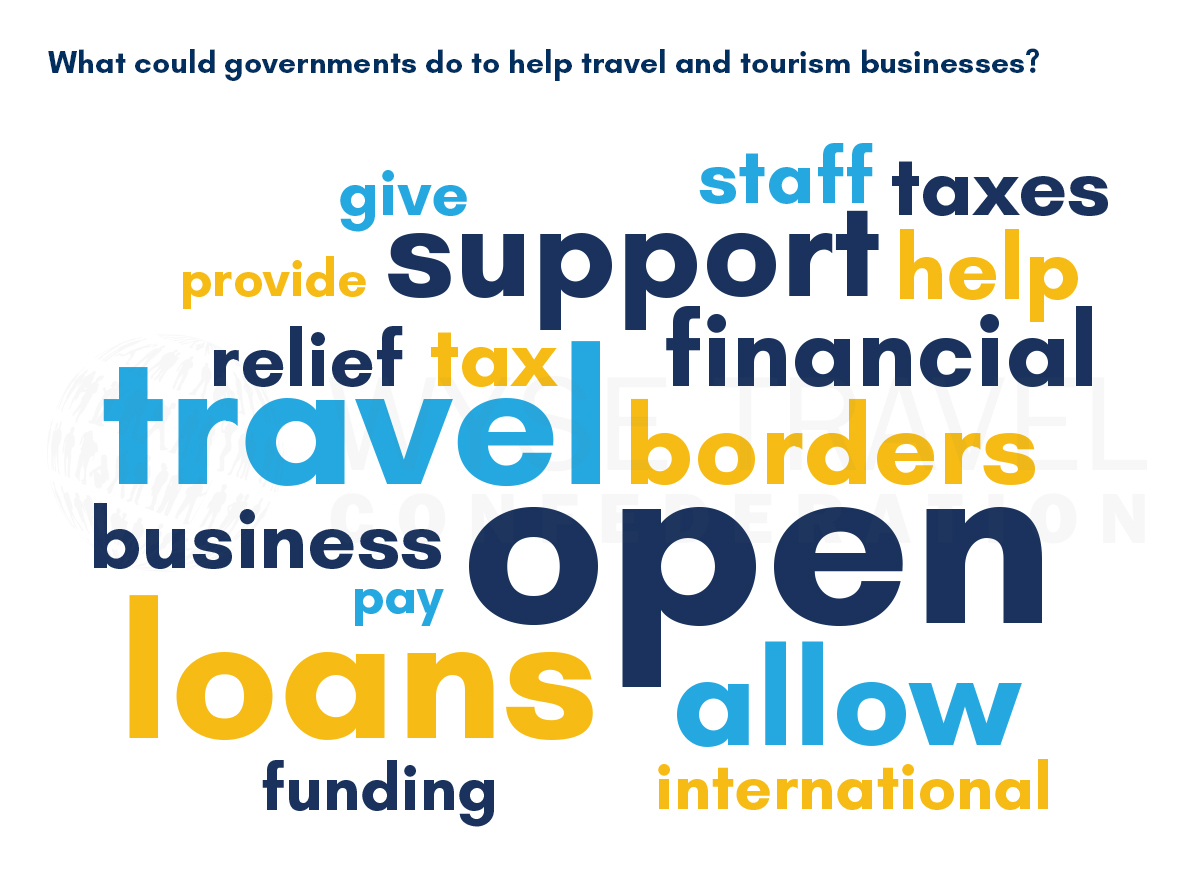

What could governments do to help travel and tourism businesses?

Respondents feel that the most important action that government could take to immediately help business prospects is to open borders for travel. Obviously without borders open for travel, businesses across the travel and tourism industry have limited opportunities. Because it is unlikely that all borders will open in the near future, businesses are looking to governments for financial assistance to see them through the crisis. The most frequent suggestions on financial support were for governments to make loans and tax relief available.

Other suggestions revolved around the themes of public health, global standards, confidence, and visas.

Funding for public health

Respondents recognised that COVID-19 represents a global health crisis, which can only be effectively tackled through government action to strengthen health systems. In the short term this should include action to increase the availability of Personal Protective Equipment (PPE), more testing and contact tracing. In the longer term, the travel industry recognises the need for a vaccine to allow customer-facing operations to return to some kind of ‘new normality’. A number of respondents also saw the need for specific improvements in health systems in travel destinations, and government measures to restore consumer confidence in travelling again. Comments about the importance of public health were most likely to come from respondents based in the USA, followed by the EU.

Establishing global standards

Some respondents underlined the need for governments to develop global standards that would help to create confidence and improve clarity for suppliers. Although closing operations down was relatively straightforward, the measures needed to enable re-opening are less clear. To provide a more level playing field, some respondents emphasised the need for common standards and clear guidelines on operation under a ‘new normal’.

Confidence

Some respondents noted that governments could help to improve business and consumer confidence by taking measures to help people navigate the COVID-19 landscape, most notably by testing and tracing and making information available to the general public and to businesses.

Visas

A number of respondents mentioned the issue of visas, which is now becoming problematic for travellers and operators. There is a need for clarity on the availability of visas and for visa application processes to be opened up as soon as possible. There was also the suggestion that there should be free visas for long-stay international students, perhaps a market that can help to provide a much-needed boost to local economies.

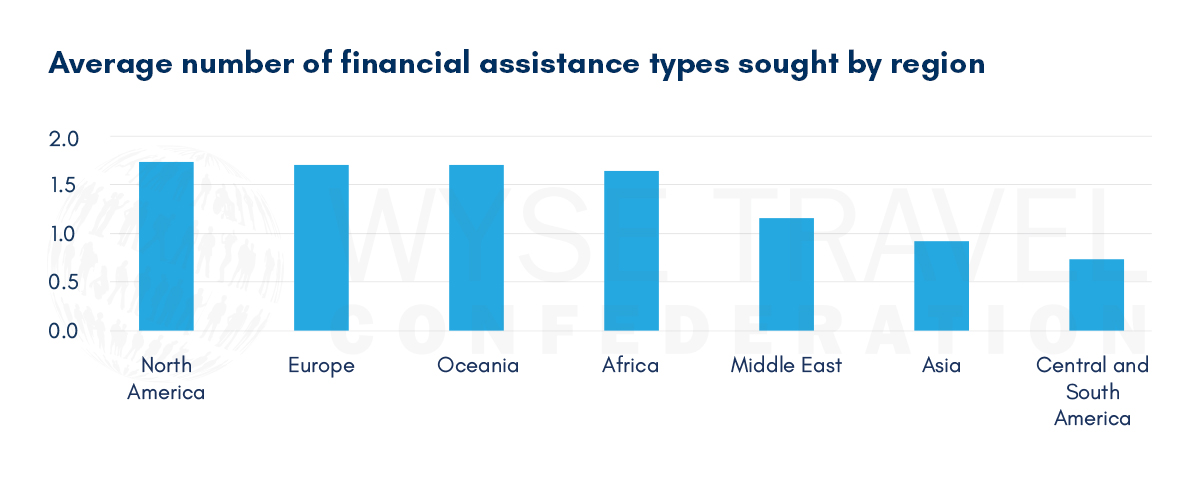

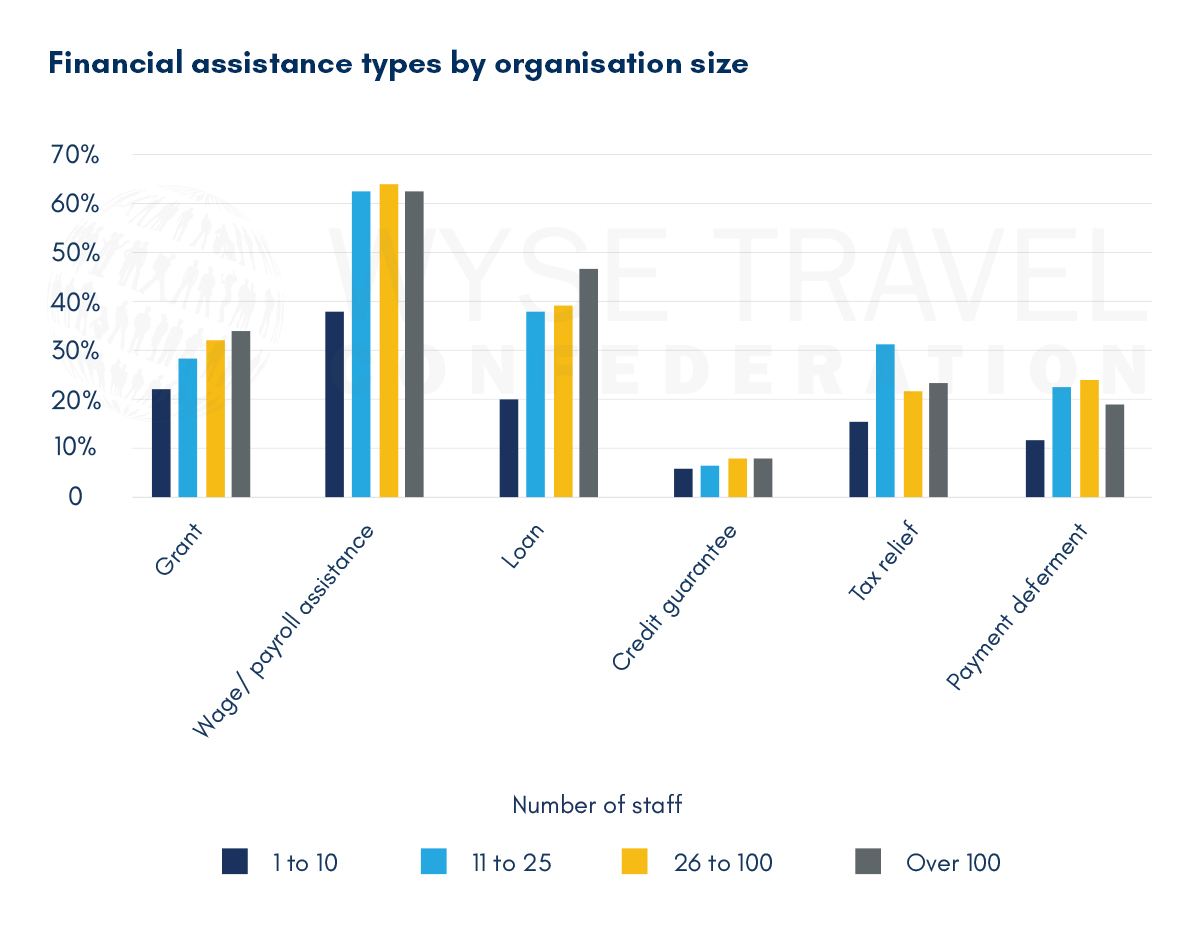

Financial assistance

In April we asked respondents to estimate how long they could keep trading without financial assistance. The average estimate was four months. This explains why a high proportion of businesses are now seeking financial assistance from government or other sources. As of May, the most common types of financial assistance sought were wage/payroll support (45%), loans (27%) and grants (24%).[2]

A significant number of respondents were seeking more than one type of financial assistance.

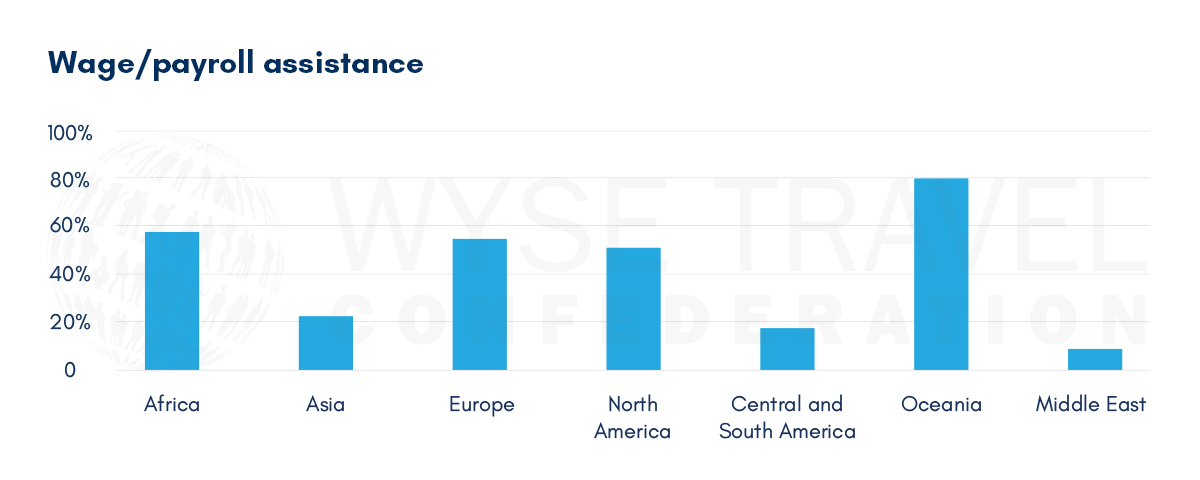

The type of assistance sought varied by region, with Oceania having the highest proportion of companies seeking wage support (80%), while this was much less likely to be requested in Asia, Central and South America and the Middle East.

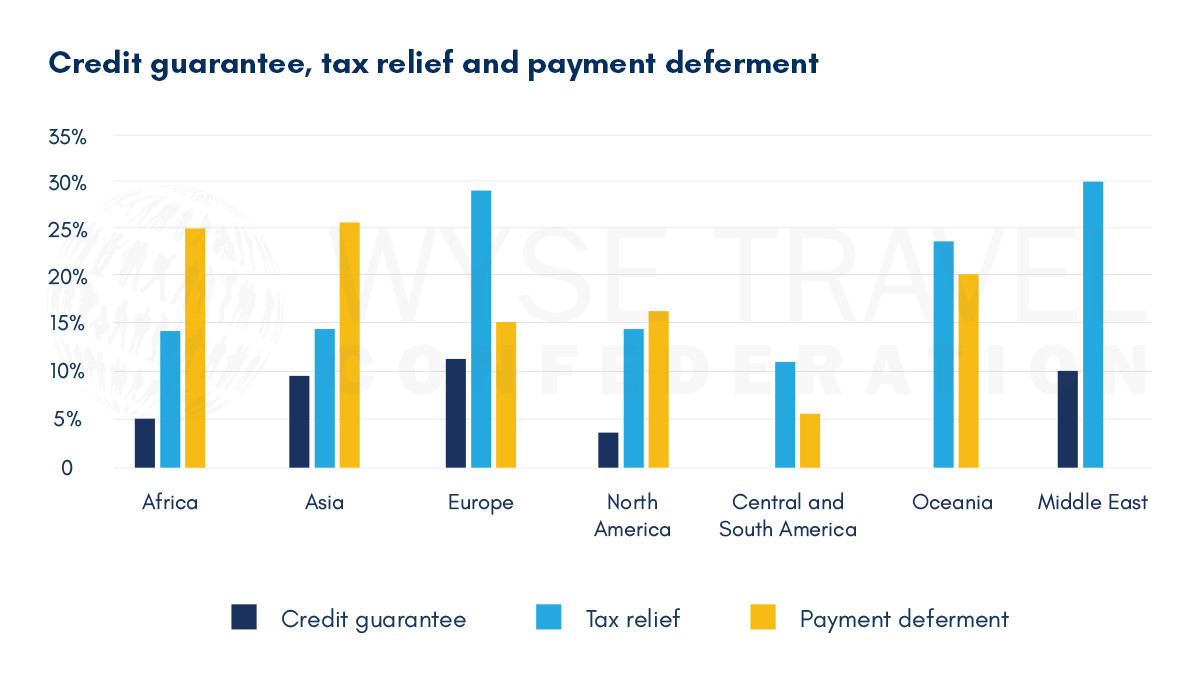

Loans were most likely to be sought be respondents in North America (44%) and the Middle East (40%), which were also regions with relatively high levels of requests for grants. In contrast, Asian respondents were least likely to have asked for either of these modes of assistance.

Of other financial assistance measures being deployed, tax relief was the most widely mentioned by respondents in May. Payment deferment was also fairly widespread, with African and Asian respondents most likely to be requesting this. Credit guarantees were most likely to be requested in Europe, whereas respondents in Central and South America and Oceania did not mention this.

Larger organisations were more likely to seek financial assistance and to request more than one source of assistance than smaller organisations.

WYSE Travel Confederation and the COVID-19 Travel Business Impact Survey

If your business would benefit from unique business insights on the youth travel market, industry representation for common business interests, and hopefully soon, new trading opportunities with international partners, we invite you to discover the resources of the global trade association for businesses serving young travellers, WYSE Travel Confederation.

Next survey in the series

WYSE Travel Confederation will repeat the COVD-19 Travel Business Impact Series 5–15 June 2020. As with past travel business crises that we have monitored, it is important for the industry to come together and take its collective temperature, so to speak. Given that youth aged 15 to 29 represent 23% of international arrivals, all travel businesses, regardless of their focus on youth-tailored travel products, are welcome to participate in the survey.

April 2020 Travel Business Impact Survey:

Q2 worse across the globe, but some source markets expecting better for the whole of 2020

Staff cuts, location closures and short survival periods

Satisfaction with COVID-19 cooperation, but placement availability concerns rise

March 2020 Travel Business Impact Survey:

Youth travel anticipating 30% decrease in business for 2020

Business outlook by youth travel sector

Looking back in order to see ahead

[1]Data for this report were collected between 1–11 May 2020 by WYSE Travel Confederation, the global association for youth, student and educational travel organisations, via web-based questionnaire (in English). The survey was the third in a series titled COVID-19 Travel Business Impact Survey. The third iteration of the survey attracted 448 responses from 71 countries. Three-hundred and forty-seven responses were retained for analysis. Respondents included organisations specialised in youth travel products as well as those representing mainstream travel products, members and non-members of the association. All respondents were asked about the impact that the COVID-19 (Coronavirus) pandemic has had on their business in travel. Questions related to change in demand, outlook for 2020, main concerns and actions taken in response to COVID-19 have been repeated across surveys. New questions related to government action, types of financial assistance and potential trends were added to the third iteration of the survey. The profile of respondents to the third survey in May 2020 was similar to that of respondents of the first and second surveys in March and April, with there once again being relatively fewer responses from language and educational travel providers and more responses from providers of accommodation and activities, tours & attractions. When comparing the May, April and March survey respondents, there has been a slight decrease over time in the level of youth travel specialisation of respondents, going from 69% in March of doing 50% or more of their business in youth travel down to 60% in May.

[2]Please note that the type of financial assistance sought by the respondent does not necessarily mean that it was actually received by the respondent.