News

Manchester, United Kingdom — 22-25 September 2009WYSE Archives

![]()

Hostels vs Poshtels: London Hostel Performance by Tier

WYSE Travel Confederation hosts global events for the youth travel industry. Click the logos below to learn more.

![]()

![]()

![]()

![]()

![]()

7 November 2019

By Kelsey Fenerty

LONDON – While market-level numbers are a good indicator of overall performance, individual property performance can vary widely depending on location, age and other such characteristics.

One such characteristic is class, the categorization of properties by Average Daily Rate (ADR). For hotel reporting, both chain and independent hotels are assigned to one of six classes based on achieved rate. While hostels have not been categorized into classes, upper and lower tiers can be approximated by looking at market ADR and separating properties according to their rate relative to market rate. Upper tier properties achieve above-average ADR and lower tier properties see below-average ADR.

As the spectrum of hostel offerings continues to expand, studying performance by tier can help operators understand what strategies and revenue management techniques may or may not be working.

What’s in a tier?

In hotels, property attributes often vary by class: a luxury hotel typically boasts amenities such as a spa, gym and restaurant, while economy properties offer little beyond a room.

For hostels in London, upper tier properties skew larger in size, offering an average of 360 beds compared to lower tier properties’ 210 beds, and are somewhat more likely to offer F&B (most often B) options to guests. Location and age are similar between upper and lower tier properties.

Revenue breakdown

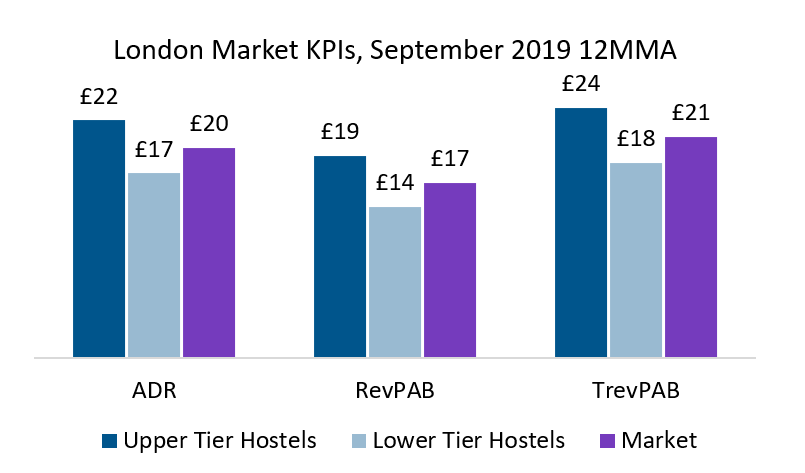

At the London market level, ADR averages £19.82, but the gap between upper tier and lower tier hostels is nearly 30% and growing: The gap measured 25% in January 2018 on a rolling 12 month basis and was 29% in the 12 months ending September.

Discrepancies in F&B and other ancillary services between the tiers appear in Total Revenue per Available Bed (TrevPAB). Upper tier RevPAB is £4.84 higher than lower tier RevPAB, but the gap between tiers in TrevPAB widens to £5.21, suggesting that amenities at upper tier properties are costlier or more frequently purchased.

Occupancy by tier

Even with rates £5 lower than upper tier properties, lower tier hostel occupancy is still below the market average. This may not be the case for much longer, however, as lower tier properties have seen strong occupancy growth in recent months, with year-over-year growth consistently outpacing that of upper tier properties.

Increasing occupancy among lower tier hostels suggests an increase in guests’ price sensitivities; while lower tier occupancy has trended up over the past two years, upper tier occupancy has remained consistently flat, bouncing around 85% on a rolling 12 month basis.

Strategizing for the future

As lower tier hostels have been driving occupancy, adding 4.5% year-over-year with a 1.0% rate increase, upper tier hostels have taken the opposite strategy and pushed rate up 4.1% from September 2019, while occupancy lifted only 0.4%.

The results are mixed. Lower tier hostels grew RevPAB the most, marking a 5.6% increase from 2018, but upper tier hostels maintained higher absolute RevPAB, at £19.09 in September 2019. While upper tier hostels outperform lower tier hostels in absolute terms, lower tier growth rates lend credence to the theory that change is on the horizon.

Interested in more?

STR reports on hostel performance in London and Amsterdam and is actively pursuing other markets. Reports are free to data providers. Interested in more information? Please contact Patrick Mayock at pmayock@str.com.

About STR

STR provides clients from multiple market sectors with premium, global data benchmarking, analytics and marketplace insights. Founded in 1985, STR maintains a presence in 15 countries with a corporate North American headquarters in Hendersonville, Tennessee, and an international headquarters in London, England. For more information, please visit str.com.

WYSE teams up with STR to provide members with insights into city performance data on hostel occupancy and bed rates.

In the first monthly report of its kind for WYSE Travel Confederation, STR’s data on London hostels show that despite average daily rates being down, occupancy remains steady.

WYSE Travel Confederation hosts global events for the youth travel industry. Click the logos below to learn more.

![]()

![]()

![]()

![]()

![]()